In the realm of global finance, discussions are increasingly centered on the looming decline of the US Dollar dominance. Given the current economic indicators — an overvalued Dollar, diminishing inflation, and the Federal Reserve nearing the end of its rate-hiking cycle — a substantial depreciation of the Dollar would typically be anticipated. However, the reality is strikingly different. The Dollar, since its peak in autumn 2022, has only seen a modest decline. This raises a critical question: Are we misinterpreting the resilience of the US Dollar?

Table of Contents

The Economic Slack Factor in Dollar Valuation

The concept of economic slack has historically been a significant indicator of the Dollar’s value post-peak. The presence of slack in an economy usually leads to uninterrupted growth with low inflation and interest rates, contributing to the Dollar’s depreciation. However, the present scenario in the US is characterized by limited slack, evidenced by tight labor and commodity markets, and consequently higher inflation. This lack of significant slack aligns more with a stable Dollar rather than a sharp decline, hinting at an extended period of relative strength for the US currency.

The Absence of Strong Rivals

In the international currency arena, the Dollar’s fate is closely tied to the relative strength of other currencies. For a significant Dollar depreciation, other major economies must present stronger currencies. However, the current global economic landscape shows no formidable challengers to the Dollar. Europe, grappling with its issues, and China, in a weaker cyclical and structural position, are not in a state to dethrone the Dollar. Even the emerging markets, despite navigating through disinflation, do not pose a substantial threat to the Dollar’s hegemony.

Investment Trends: A Pillar of the Dollar’s Valuation

The continuous flow of capital into US assets has been a key factor in maintaining the Dollar’s high valuation. Despite talks of de-Dollarization, the US remains an attractive destination for investors, primarily due to the high ‘risk-free’ yields and the allure of the tech sector. This steady influx of capital has played a critical role in propping up the Dollar, countering forces that would typically drive its value down.

The Dollar’s Shallow Depreciation and Diverse Performance

Given the resilient economic picture in the US and the lack of clear global challengers, the Dollar is expected to follow a trajectory of shallow depreciation. This trend is marked by a differentiated performance in the currency market. While currencies like the Swiss Franc and Canadian Dollar, as well as some higher-yielding emerging market currencies, may see tactical appreciation, other major currencies are likely to lag behind. This differentiated performance underscores the complexity of the current currency landscape and the unique position of the Dollar within it.

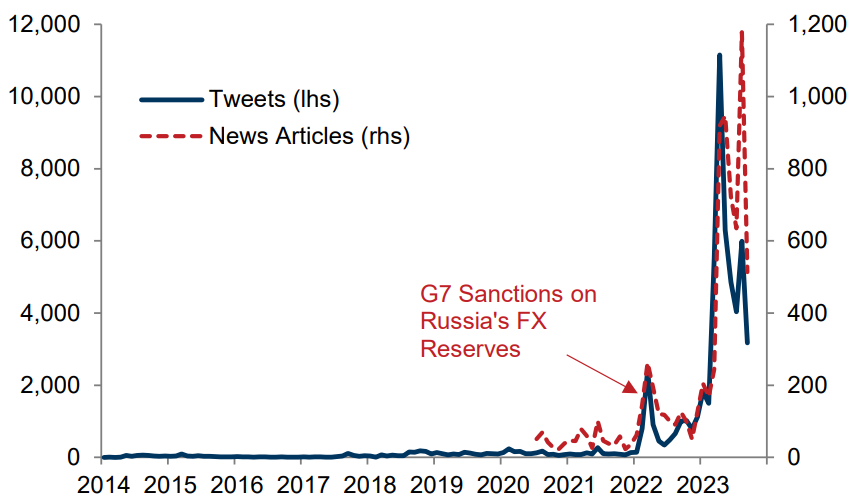

De-Dollarization: Rhetoric Versus Reality

The concept of de-Dollarization has been a topic of considerable discussion in the current geopolitical context. However, the practical implementation of moving away from the Dollar has been limited. Only a few countries have made real strides in this direction, with mixed results. The private sector continues to favor Dollar assets, further reinforcing its high valuation. This gap between the rhetoric and the actual implementation of de-Dollarization strategies suggests that the Dollar’s dominant position in the global financial system is unlikely to change in the near future.

The Overstated Demise of the Dollar

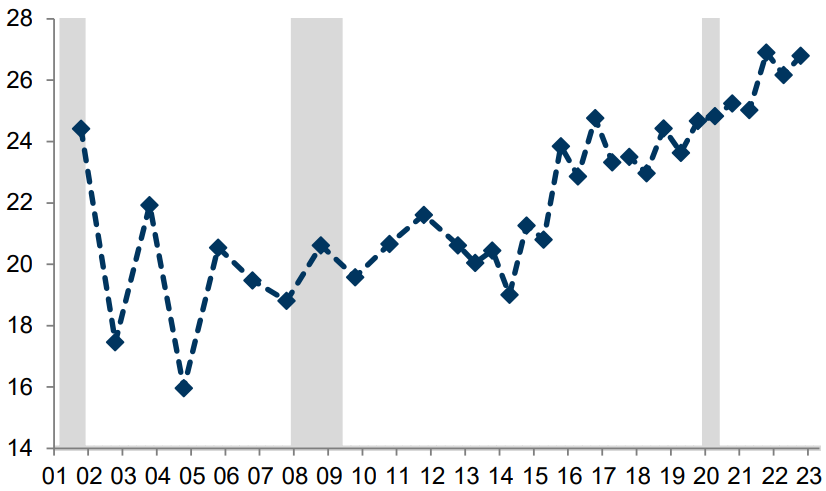

The narrative surrounding the Dollar’s decline has often been exaggerated. While cyclical factors like the end of the Fed’s rate-hiking cycle have historically aligned with a weaker Dollar, the US currency has maintained its strength. This persistence is partly due to the influx of capital chasing ‘US exceptionalism,’ particularly in the last decade, which has seen significant US equity returns. These inflows, along with the strong relative performance of US assets, have increased the share of US assets in global portfolios. Notably, much of this capital has originated from areas like the Eurozone and Japan, where low rates and weak growth have repelled investors.

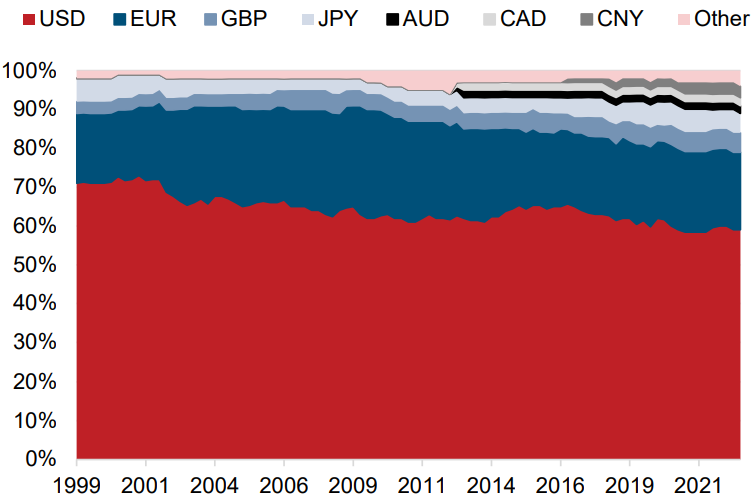

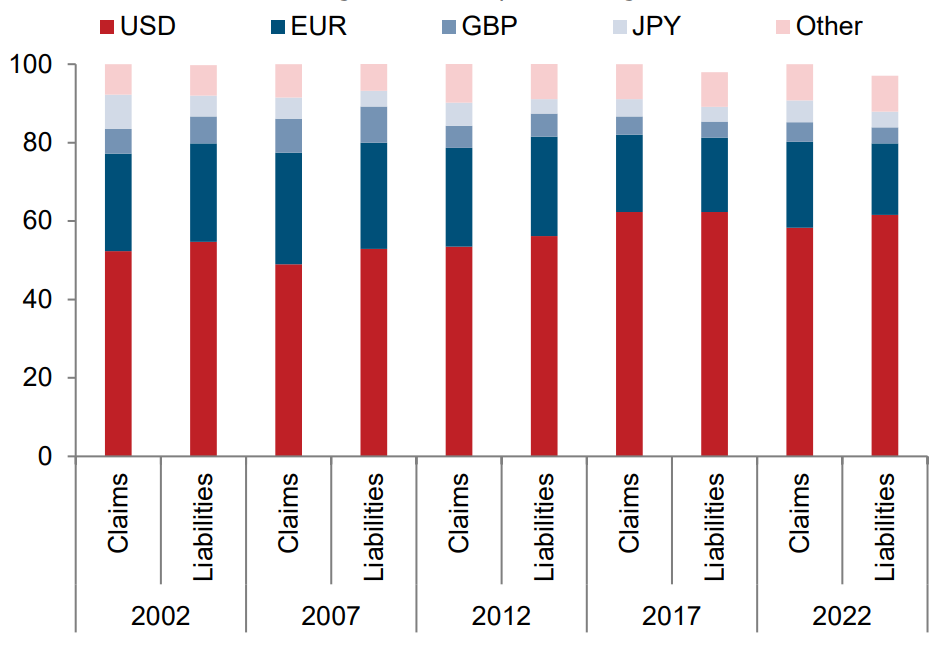

The Search for Alternatives to the Dollar

Despite the declining share of the Dollar in global FX reserves, it remains the predominant reserve currency. The search for higher returns has led to diversification into currencies like the Australian and Canadian Dollars, yet none have challenged the Dollar’s supremacy. Reserve managers prefer currencies that are liquid and reliable, especially in risk-off scenarios, a niche that the Dollar continues to fill effectively.

US Dollar Dominance Set to Persist

Looking ahead, based on all the above reasons, the end of the Dollar’s dominance as the global reserve currency seems contingent on better capital returns from other economies and more profound structural changes in the global financial landscape. These changes would require deeper capital markets outside the US and significant shifts in the composition of reserve assets.

Given all the presented factors, we can state: the US Dollar will maintain its position as the global reserve currency for the foreseeable future.